.svg)

What is open banking?

In a few words - it’s a financial services term as part of financial technology that refers to:

- the use of open APIs that enable third-party developers to build applications and services around the financial institution;

- greater financial transparency options for account holders ranging from open data to private data.

In more detail, it is a result of a series of reforms in the banking sector, which defined how our banking data should be handled and shared. The result of these changes mean that the banks on the UK and EU market are now obliged to share that data with us and whoever we authorize to use them however we like! At the same time, the security of this process is also now monitored by these institutions as per the guidelines included in the reforms.

The implementation of this solution on the market enabled to use financial data from our bank (spending habits, current balance, historical balance, etc.) in other digital products - apps, payment gateways - while at the same time being sure that they don’t really leave our account and are still safe. Thanks to using the API technologies, we can share only this part of data which are needed for a given objective - so for example, if we want a particular service to access only credit card information, then it won’t be able to access our checking account balance.

The introduction to API

Of course, Open Banking is not obligatory! If we don’t want to share information with anyone, we don’t have to. The data are still secure in the banking system, as they were before.

What was the idea behind open banking?

The birth of this project is a consequence of two separate factors.

In 2016, in the UK, the Competition & Markets Authority completed the traditional retail banking assessment and the market was deemed not innovative enough and due to low competitiveness, the costs of their services were growing. This was the foundation to build a solution, which would allow third parties to access the banking data of any user in order to process them in any new way and change the approach to financial products, applications, and services.

Another factor was The Revised Payment Service Directive, better known as PSD2 regulation pushed by the EU - from the idea formed in 2013 up to implementation at the end of 2018. Other countries and whole regions across the world didn’t lag behind legislating proper laws to establish an environment conducive to the rise of Open Banking.

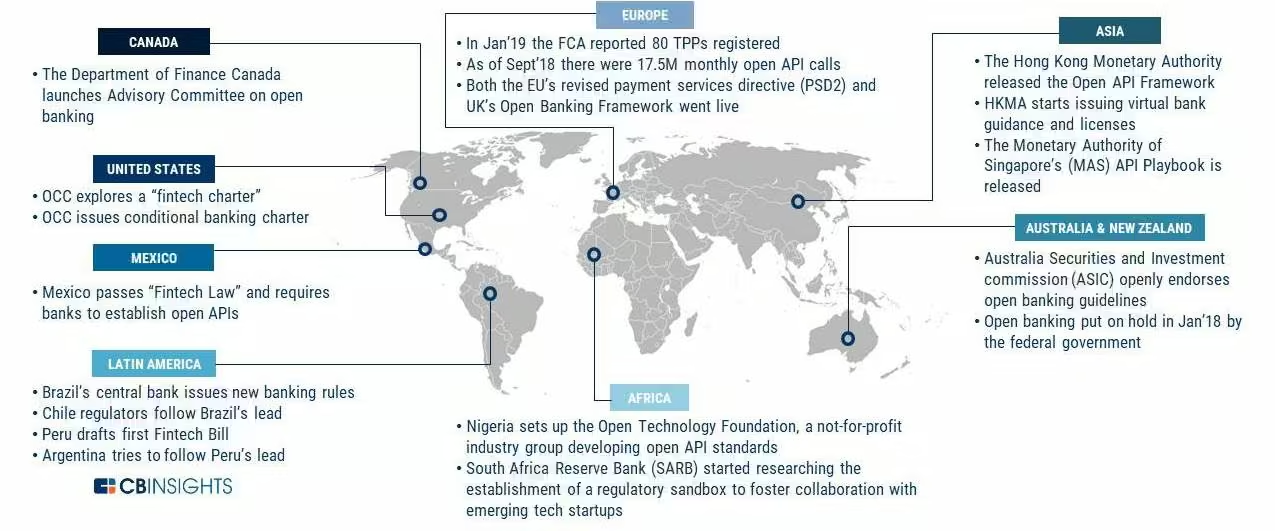

Solutions enabling open banking across the world, source: paymentscardsandmobile.com

The concept was pretty the same - to create a universal, safe way for customers to share their banking information with selected, trustworthy applications and services in order to keep the data both - secure and accessible.

The client’s financial data were released from under the monopoly of the banking system and given back to clients.

But that also sparked the rise of innovative startups in that business. The global financial platform based on APIs created under the unified set of rules was created, which gave the same position to neobanks (like Revolut or N26), fintech and traditional banks. This move worked, it did disrupt the market and led to lots of innovation in the whole industry.

How does Open Banking work?

As the solution has been built as an API you can easily access the data, which your users would be kind enough to share with your app. This has created (or refreshed) quite a few product concepts:

- savings applications, which monitor your spending habits and even suggest areas of improvement of your financial condition,

- the all-in-one money management system, where you can connect all your accounts, credit cards, etc. and be able to check your current balance at one glance,

- the investment applications of all kinds - allowing you to buy and sell your investment vehicles from your investment accounts using independent advisors,

- the credit or insurance application, gathering all necessary data to apply for a policy and comparing offers available on the market,

- you tell me!

Being ubiquitous, Open Banking opened a lot of possibilities, which were previously only available for big, established banks. Of course, companies that build fintech and neobank solutions are still monitored and in most of the markets, you need to acquire a license or approval from the responsible organization or institution. But the leaders of this new charge have more similarities with tech start-ups from Silicon Valley, than with the traditional banks, which are not really synonymous with innovation. And that’s where the advantages of the latter actors - client base, brand, established market position - are being slowly lost.

No more screen scraping: At the very beginning, apps harnessing Open Banking required users to provide the same username and password used to log in to their bank accounts. Then, the app would “screen scrape” the information it needed. This technology has been dropped as it was deemed not secure and effective enough.

Is Open Banking secure?

Another idea behind Open Banking was to limit fraud on the B2C banking market. Before this was put in place, there were numerous examples of complex techniques aimed at consumers, which resulted in capturing log-in data for bank systems, exposing consumers to the risk of losing access to their accounts and, of course, money. This was also one of the main points addressed by PSD2 - for example by forcing banks to use two-factor authentication, changing the characteristics of online sessions (for example reducing the single log-in session time) and urge users of contactless cards to authorize with PIN more frequently than before.

But how are users able to know if it is secure to use apps, which employ this solution? To answer this question, we have to consider two aspects.

Firstly, not every application is worth the trust.

In order to verify the credibility of a particular app, users can check if the institution behind it is being registered and approved by Financial Conduct Authority (FCA) in the UK or European Banking Authority in the EU.

If the provider is not listed there, it’s hard to recommend its services. The FCA also gives a chance to check if the company has been known to be a fraudulent entity - they are listing all known scam companies on this list.

Second thing is that APIs are a safe solution - by definition, they don’t allow the recipient to access any data it’s not supposed to, it doesn’t allow the app to read any of the log-in details and the user can withdraw the permission at any time. So even if the company is not listed in the register, the data should be secure - but it’s better to be safe than sorry.

Examples of utilising Open Banking - outside of banks and fintech

Your financial data are a powerful tool. As banks and other financial institutions are one of the most trustworthy sources of information, the data held by them could be used for other identification purposes. This led to the creation of a project called Known Traveller Digital Identity, established by the World Economic Forum. The idea is simple - using your smartphone with an app, verified by your banking data, would be able to replace a traditional passport. Even now, some of the countries are already using the contactless feature to identify the citizens with a digital form of passport - with photo, all the ID data, and fingerprints embedded into a chip. So why not use the verified app holding all the same data? The work is ongoing, but this might be closer than we think.

Another idea is to help customers find a perfect apartment for them to live in. Everyone knows how hard it is to find a spot that fits your needs - shops, schools, maybe preferred bank? Everyone likes to have these institutions in their vicinity. There’s a possibility of creating an app, which would analyse your spending habits and suggest the estates that are placed near as many spots you need as possible. Sounds like science fiction? That’s possible more than ever with the access to your banking info through Open Banking API.

The last example of the non-obvious use of banking data would be to monitor the wage gap between genders in any given profession. Imagine an app, where you’d add your banking data, your line of work and your gender, and the algorithm would calculate an average difference between men’s and women’s salary in a given business. That would open the discussion on the ground-level regarding payment fairness around the world. And it will be calculated on a reliable set of data. Would you be willing to join such a movement?

What does your business need to do to be successful with Open Banking?

There’s a number of success factors in fintech app development but the first tip is to become business- as well as client-oriented. Up to the point of Open Banking introduction, banks were concentrating too much on their products, their offer and additional upselling through their internal channels, instead of the comfort and benefit of the client. Now, when there’s an “outside” competition and customers don’t have to log in to the bank's systems anymore. They are starting to develop new solutions, aimed at making customers feel more at home in their environment. That’s crucial because the weight has shifted - from institution-owned data to client-owned data. And the clients might use this data wherever they want, wherever it’s more convenient for them.

Why User Experience is crucial in fintech apps?

These are two things that you should focus on to make your solution stand of the crowd - UX/UI design and original features. Your app should be easy to use and intuitive enough to be the main product for customers on the market you’re aiming for. Open Banking has given a lot of companies a room to grow and be creative - but if your app is hard to use or decipher, users will give it a wide berth. Therefore focus on the design and clarity of features would be crucial to get through to your target user.

Your browser doesn't support HTML5 video.

Home buget app design. See more examples of fintech designs on our dribbble.

Another aspect is to make sure that you’re not building a too complex (thus complicated) app. Providing users with insurance buying possibilities, bank accounts monitoring, savings advice, and real estate buying suggestions might be too hard to pack into one app without losing track of what’s important. The multitude of information would impact the ease of navigation - therefore complicating the User Experience and User Interface part of work on the app. Make sure that you know where the Unique Competitive Advantages of your product lie and focus on these. It would be great to make sure that your product design team is experienced and has a great track record of creating products, which are successful in the market! Working with experts gives your business a bigger chance to make an impact on the market, so that’s definitely a thing to consider when planning a launch.

Online product design workshops to start the remote collaboration

The last thing to consider is to think about the unique experience your app would deliver to the customer. Remember that Open Banking gives the same possibilities to every developer and business. So if your company wants to make an impact on the market, there has to be something exceptional about it - either features, ease of use, or other advantages (low cost? Competitive offer in the segment you’re aiming for?). You need to make sure that your offer is one-of-a-kind and get ready to create a ripple effect.

Looking for a reliable partner in developing your open banking product? Check how we helped mobile banks, the providers of wealth management apps and solutions for DIY investors and talk with us to see how we can support your project!

.svg)

.svg)

.svg)

.avif)

.avif)

.avif)

.avif)